Zee Entertainment Enterprises Ltd (ZEE) shares have plummeted by 56% from their peak in December 2023, when they reached Rs 299.50 per share. This decline has severely impacted retail investors, primarily due to the breakdown of the media company’s merger with Sony earlier this year.

Although the management and board of ZEE have initiated a comprehensive strategy to restore its former success, Emkay Global’s latest analysis suggests that achieving a performance level similar to that seen during FY13-19 will be challenging, given the shifts in industry dynamics.

According to this brokerage, short-term performance is anticipated to deteriorate further due to these interventions before any improvement is observed in ZEE’s situation. Emkay Global expressed concerns about ongoing legal challenges potentially disrupting current plans. While the current valuations appear favourable, Emkay Global believes a comprehensive re-evaluation is only likely if a new partner or buyer emerges.

As of March 31, there were a total of 611,394 individual investors holding shares in the company, with nominal share capital of up to Rs 2 lakhs. Collectively, they owned a 22.97% stake in the media company by the end of the fourth quarter.

Emkay Global has revised down its estimates for ZEE’s EBITDA for FY25-26 by 10-12%, factoring in a slower recovery. Despite a sharp 24% correction since their last report and limited downside potential from current levels, Emkay Global has upgraded its rating on ZEE to Reduce but maintains a negative stance. They have adjusted their target price to Rs 150 per share (8x Mar-26E Broadcasting EBITDA).

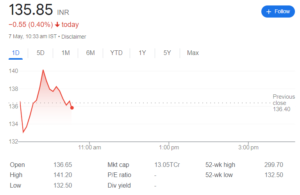

On Tuesday, ZEE shares were trading at Rs 136.95, up 0.22%. Emkay Global’s target price suggests a 9.52% potential upside over this price. The broking firm said its near-term performance is likely to further deteriorate from current levels as it implements measures to achieve its FY26 targets.

near-term performance is likely to further deteriorate from current levels as it implements measures to achieve its FY26 targets.

Zee’s Operational Challenges

Zee5, which has been driving down the margins of the entire company, can be impacted and see some slowdown in revenue as the focus now shifts more toward reducing the losses. Also, the company’s legal woes continue about the merger-related case with Sony, its tussle for cricket rights with Disney Star, and Punit Goenka’s ongoing SEBI case.

“Any unfavourable decisions against the company could cause further pain and derailment of current plans, in our view. We believe the company is up against a tough business environment currently, and particularly with it competing against the larger entity of Disney- Reliance combined,” it said,

It has withdrawn its merger implementation application filed before the NCLT, to pursue growth and strategic opportunities. Emkay said the emergence of a new partner would be a key trigger for a stock re-rating.

“The stock is currently trading at its lowest valuation since the last 10 years (on a 1YF EV/ EBITDA basis), which is a clear sign of the tight spot it is in. The stock price has sharply corrected since the merger breakoff, and could continue to languish given the lack of triggers in the near term,”

On Tuesday, ZEE shares were trading at Rs 136.95, reflecting a marginal increase of 0.22%. Emkay Global’s target price suggests a potential upside of 9.52% from this price level. The brokerage firm anticipates a further deterioration in ZEE’s short-term performance as it undertakes measures to meet its FY26 targets.

The profitability of Zee5, which has been exerting pressure on the company’s margins, might witness a slowdown in revenue growth as efforts intensify to minimize losses. Additionally, It continues to grapple with legal challenges related to the failed merger with Sony, its dispute over cricket rights with Disney Star, and Punit Goenka’s ongoing SEBI case.

Withdrawal of Merger Application and Prospects for a New Partner

Emkay Global warns that adverse rulings in these legal matters could exacerbate the company’s difficulties and disrupt current strategies. ZEE faces a challenging business environment, especially with competition from the larger Disney-Reliance entity.

ZEE has opted to withdraw its merger implementation application filed before the NCLT to explore growth and strategic opportunities independently. Emkay Global highlights that the identification of a new partner could serve as a significant catalyst for a re-rating of the stock.

The current valuation of ZEE is at its lowest in the past decade, based on a 1-year forward EV/EBITDA basis, indicating the significant challenges it faces. The stock price has witnessed a sharp decline since the merger breakdown and could continue to stagnate due to the absence of immediate positive triggers.

Also Read: Zee Entertainment Plans 15% Workforce Reduction; Embarks on Cost-Cutting Measures

{kind=link}